The Fed Stress-Tests Banks This Week — Here's the Stress Test Most Banks Are Failing

This Wednesday, the Federal Reserve publishes the results of its annual bank stress test, the yearly checkup that simulates how 32 large banks would hold up under broad economic shocks. A day later, on Thursday, the Fed gets fresh inflation data from its preferred gauge, the personal consumption expenditures price index — its first read on prices since holding interest rates steady and signaling a possible hike later this year. It's a week built around a simple question that defines modern banking: can these institutions withstand pressure they can't fully control?

That's the right question to be asking — and not just about capital ratios. Because there's another stress test running on banks and financial institutions right now, one with no published results and no regulatory deadline, that a large share of them are quietly failing. It's the test of whether your institution shows up — accurately, consistently, credibly — when a customer asks ChatGPT, Perplexity, or Gemini which bank, credit union, or financial product they should choose. The Fed's stress test measures resilience against a financial shock. This one measures resilience against a discovery shock: the rapid shift of customers from Googling financial products to simply asking an AI. And for institutions whose digital presence was built for the old world, the results aren't pretty.

This piece looks at why AI search has become a real stress test for financial institutions, what the early data reveals about who's passing and who's failing, and what banks and credit unions can do to shore up the visibility that increasingly determines who wins the customer.

Customers are asking AI before they ever reach you

The behavioral shift underneath all of this is already mainstream, not emerging. Nearly 60% of consumers polled by J.D. Power in late 2025 said they occasionally use AI for banking and financial services, and 13% said they do so every day. A global Cognizant study scored consumer willingness to use AI to learn about banking and financial products at 90 out of 100 — one of the highest of any category. Research cited by The Financial Brand found that consumers under 45 now use large language models as the second-most-used channel for researching financial institutions, trailing only traditional search engines.

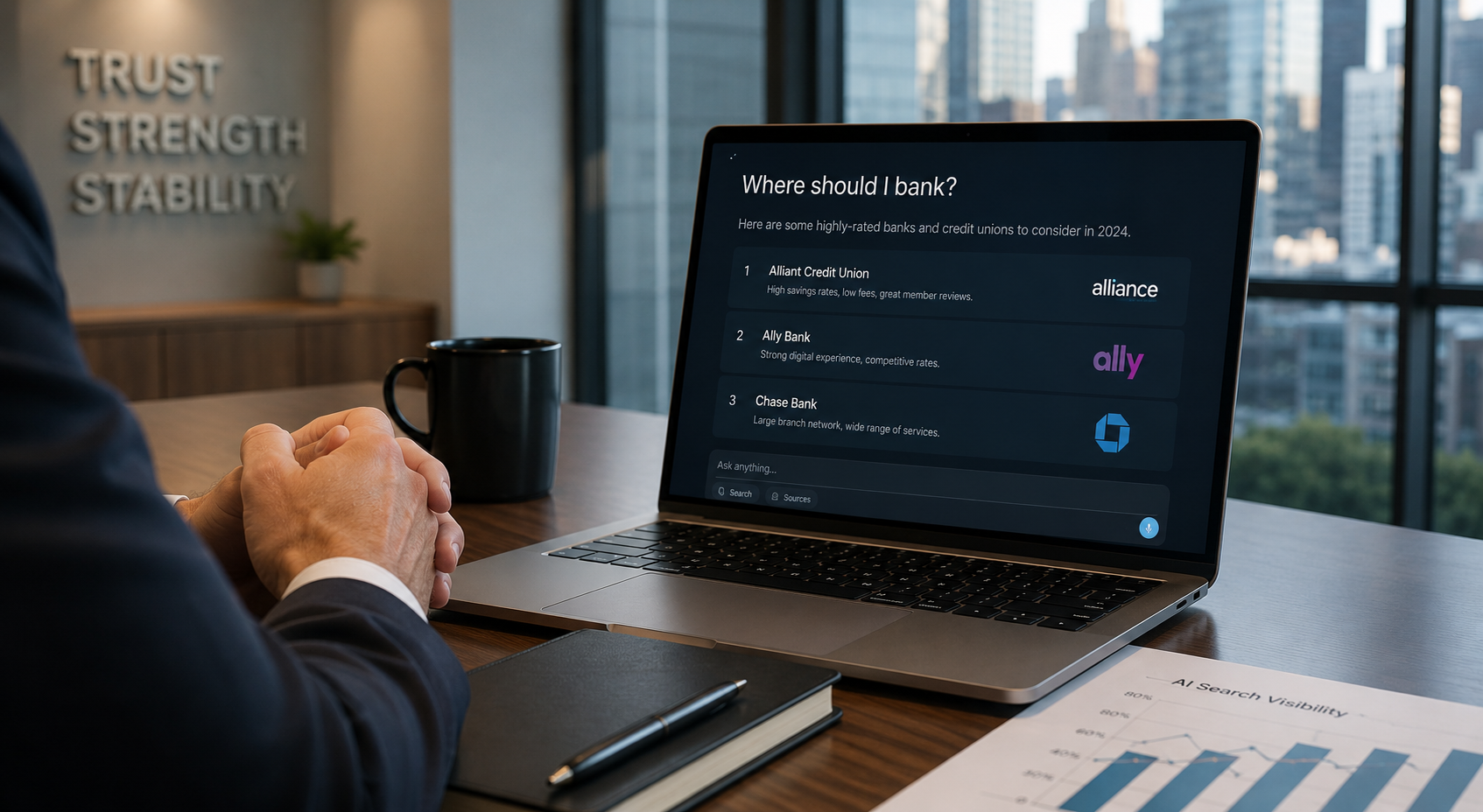

The questions these customers ask are specific, high-intent, and exactly the kind that used to lead to a branch visit or a rate-comparison page: "What credit union has the best auto loan rates near me?" "Do I qualify for a HELOC if I'm self-employed?" "Which bank makes it easiest to open an account as a young parent?" The AI answers directly — and because answer engines no longer return long lists of links, they surface only two or three institutions. As one industry analysis put it, the place where your next customer first encounters your institution has shifted fundamentally: prospects ask AI for financial guidance before they ever visit a website, call a branch, or click an ad, and the institutions that appear in those answers capture that first impression and the trust that comes with it.

The danger, as with the Fed's adverse scenarios, is that the failure is invisible until it's material. A prospective member who asks an AI about local auto loans, never sees your institution in the answer, and goes with a competitor leaves no trace in your analytics. The absence doesn't show up on a dashboard — it shows up, eventually, in your membership and deposit numbers. By then the stress has already done its damage.

The early results are in — and size isn't saving the big banks

Unlike the Fed's test, the AI-visibility test has already produced a public leaderboard, and it's revealing. eMarketer's AI Visibility Index for financial services analyzed thousands of ChatGPT responses across nine product categories using real consumer-style prompts. The headline finding upends conventional assumptions: the same handful of brands consistently surface in AI answers, and they are not always the largest institutions.

The specifics are striking. In the auto loan category, SoFi led at a 34% mention rate, with Navy Federal Credit Union right behind at 33.6% and Bank of America at 31% — a five-point spread between first and fifth, the narrowest of any category, meaning the rankings are still genuinely up for grabs. Fintechs often dominated their categories outright: Klarna was recommended in 91% of buy-now-pay-later queries. The research's clearest lesson is that visibility in AI recommendations depends less on size or advertising spend and more on trust, clarity, and customer relevance. As eMarketer's analyst summarized it, the brands that perform best are the ones with very little ambiguity around who they are, what they stand for, and what they should be recommended for.

This is the part that should worry large institutions and encourage smaller ones. Decades of brand recognition and enormous ad budgets don't automatically translate into AI visibility. An institution that markets itself as everything to everyone — the traditional big-bank posture — performs worse in an AI environment than a focused competitor with clear positioning and clean data. The stress test doesn't reward size; it rewards clarity. And that levels the field in a way traditional marketing never did, giving community banks, credit unions, and fintechs a real shot at being the answer.

Why financial institutions are especially exposed

Several features of banking make this stress test particularly demanding for financial institutions specifically.

The trust bar is higher, and so is the cost of error. Financial content has always been held to a higher standard — Google's YMYL ("Your Money or Your Life") classification recognizes how much harm wrong financial information can cause. AI engines apply a similar elevated bar, drawing on explainers, comparisons, risk disclosures, and guidance from across the ecosystem rather than just a bank's own pages. Misinformation about a financial product carries real consequences, so the engines lean toward sources they can parse clearly and trust confidently. Institutions with thin or inconsistent data give the AI reasons to look elsewhere.

The content style banks built for Google can work against them in AI. Financial institutions spent years producing long, comprehensive content to satisfy YMYL standards. But that dense, brand-forward style can hurt citation in AI engines, which prioritize clarity, structure, and direct answers. A page that opens with "Experience the difference of member-first banking" and buries the actual loan terms three scrolls down tells an AI nothing useful. The engines want self-contained, citable chunks — a clearly stated question, a direct answer, and supporting data — not marketing prose with the facts hidden inside.

Much of what AI cites isn't even your website. Research on how models source financial answers found that across most major AI tools, more than 60% of citations came from publishers or affiliate sites rather than the financial institutions themselves. Different engines behave differently — Gemini leans more on institutions' own pages, while ChatGPT, Perplexity, and Copilot draw heavily from independent publishers and experts — which means a single visibility strategy won't work across all platforms. The content ecosystem around your brand now matters as much as your own site, and institutions that have ignored third-party presence are exposed across the board.

How AI decides which institutions to recommend

Understanding the mechanism turns this from an anxiety into an action plan. When a customer asks an AI for a financial recommendation, the engine interprets the intent behind the question, evaluates trust signals, and determines which institutions most closely align with the described need. It's not matching keywords to product pages; it's reasoning about who fits. That's why clarity of positioning matters so much — the institution that has defined exactly who it serves and what it's best for is the one the AI can confidently slot into a specific query.

Trust signals carry enormous weight, and they extend well beyond your website. The institutions that appear most consistently in AI recommendations tend to have strong customer satisfaction, positive reviews, high engagement, and broad visibility across third-party channels. AI systems absorb signals from social conversations, customer sentiment, and external digital activity to gauge which institutions feel relevant and credible. Recency matters too: a rates page untouched for four months, a product page with outdated terms, or a news section that went quiet years ago all signal to the engines that your information may be unreliable.

And the technical foundation determines whether the AI can read you at all. Schema markup tells AI systems what a page actually contains — that a rates table is a rates table, that an address is a location, that a loan page is a product. Without it, the AI has to guess, and in financial services, guessing is precisely what you don't want. Structured, machine-readable rate data, clearly labeled and dated ("Auto Loan Rates: 6.5% APR, effective June 2026"), lets an AI extract and cite specific figures accurately — which serves both your visibility and your regulatory accuracy.

How to pass the AI stress test

The remediation playbook is concrete, and it maps to the same logic the Fed applies: identify the weaknesses, then strengthen the foundation before the shock hits.

Answer the real questions directly and on their own pages. Every prospective customer has the same core questions — who can join or qualify, how to apply, what it costs, how long approval takes, what the rates are. Answer each one directly, in plain language, on a clearly written page rather than scattering the information across your About section, FAQ, and application flow. AI engines prioritize content that can be extracted as a complete, self-contained answer to a specific question. Write for how customers actually phrase their needs ("a bank that makes opening an account easy"), not just for product taxonomy.

Fix the technical and data foundation. Implement schema markup so AI can interpret your rate tables, product pages, and locations. Keep rate and product data current and clearly dated. Maintain a single, structured source of truth for figures that change, which helps both AI accuracy and compliance.

Build credibility across the ecosystem, not just on your site. Since most AI citations in finance come from third-party sources, your presence in credible publications, comparison sites, and structured directories matters as much as your own pages. Cultivate reviews, customer sentiment, and authoritative mentions, and keep them fresh. Define your institution as a clear, consistent entity everywhere an AI might look.

Sharpen your positioning. The single biggest differentiator in the AI Visibility Index was clarity. Decide what your institution is genuinely best for and who it serves, and make that unambiguous across your content. Ambiguity is what gets you left out of the answer.

Measure AI visibility as a real KPI. Audit how often and how accurately you appear across ChatGPT, Perplexity, Gemini, and Copilot for the prompts your customers actually use. Track "AI visibility share" the way you've tracked search rankings, watch for branded-search lift as a downstream signal, and re-test after major AI updates. You can't manage a stress test you don't measure.

The encouraging reality is that, like the Fed's test, this one is passable with preparation — and unlike the Fed's, the standards reward focus over scale. Early movers are already building citation authority that late movers will find expensive to close.

The bottom line

The Fed will tell us Wednesday how 32 big banks would weather a hypothetical financial shock. But every financial institution, large or small, is already being tested against a very real one: the shift of customers to AI as their first stop for financial guidance. The early results show that visibility in AI answers isn't bought with the biggest budget or the oldest brand — it's earned with clarity, clean data, credible third-party presence, and content that directly answers what customers ask. Institutions that shore up those foundations now will be the ones surfaced when a prospect asks an AI where to bank. Those that wait will discover their failure the way the Fed's adverse scenarios play out: invisibly at first, and then all at once, in the numbers that matter. The question isn't whether your customers are asking AI which institution to choose. It's whether yours can pass the test when they do.

Frequently Asked Questions

Are people really using AI to choose banks and financial products?

Yes, and it's already mainstream. Nearly 60% of consumers told J.D. Power in late 2025 they occasionally use AI for banking and financial services, with 13% using it daily, and a Cognizant study scored consumer willingness to use AI for financial products at 90 out of 100. Research also shows consumers under 45 now use AI tools as their second-most-used channel for researching financial institutions, behind only traditional search. They ask specific questions — best auto loan rates, HELOC qualification, easiest account to open — and act on the AI's direct answer.

Does my institution's size and brand recognition protect its AI visibility?

No — and this is one of the most surprising findings. eMarketer's AI Visibility Index, based on thousands of ChatGPT responses across nine financial categories, found that the brands surfacing most consistently aren't always the largest institutions. Fintechs and credit unions frequently outperformed big banks in their categories. Visibility depends less on size or ad spend and more on trust, clarity, and customer relevance. Institutions that market themselves as everything to everyone tend to perform worse than focused competitors with clear positioning.

Why are financial institutions more exposed to this than other businesses?

Because the trust bar is higher and the content dynamics are tougher. AI engines apply an elevated standard to financial topics (the equivalent of Google's YMYL classification), drawing on explainers and comparisons from across the ecosystem. The dense, brand-forward content many banks built for Google can actually hurt AI citation, which rewards clear, direct, structured answers. And in finance, research shows more than 60% of AI citations come from third-party publishers and affiliate sites rather than institutions' own websites, so your broader content ecosystem matters as much as your site.

How do AI engines decide which institutions to recommend?

They interpret the intent behind a customer's question, evaluate trust signals, and match the need to the institution that best fits. Trust signals include customer satisfaction, reviews, engagement, recency of content, and visibility across third-party channels — not just your website. Technically, schema markup and clearly structured, dated rate and product data let the AI read and cite you accurately. Clarity of positioning is decisive: the institution that has defined exactly who it serves and what it's best for is the one the AI can confidently recommend for a specific query.

My website ranks well on Google. Isn't that enough?

Not anymore. Traditional ranking authority and AI visibility are increasingly separate signals — AI engines often cite sources from outside the top organic results and pull heavily from third-party publishers. A strong Google ranking doesn't guarantee you appear in the two or three institutions an AI surfaces. And because AI answers are frequently zero-click, customers may form their entire impression and shortlist without ever reaching your well-ranked page. You need to be in the answer itself, not just on the results page.

What's the first thing my institution should do?

Find out where you actually stand. Audit how often and how accurately you appear across ChatGPT, Perplexity, Gemini, and Copilot for the real questions your customers ask — best rates, qualification, account opening, comparisons in your market. That baseline shows whether you're surfacing, being skipped, or being described inaccurately, and which gaps to close first. From there, prioritize fixing direct-answer content, schema and rate-data structure, third-party presence, and positioning clarity.

Is AI search optimization a quick fix or an ongoing effort?

Both, in layers. Technical fixes — schema markup, structured rate data, direct-answer pages — can be implemented relatively quickly and remove the barriers that make you invisible. But the durable drivers, like third-party credibility, customer sentiment, content freshness, and citation authority, compound over months, much like SEO. AI engines also update regularly, so visibility needs ongoing monitoring and periodic re-testing. Early movers are building citation authority now that later movers will find harder and more expensive to close.

When a customer asks ChatGPT or Perplexity which bank, credit union, or financial product to choose, does yours show up — and is it described accurately? Most institutions have no idea. Ritner Digital builds the content, structured data, and authority that get financial institutions found and cited correctly across Google, ChatGPT, Perplexity, and Gemini — then we publish our own data to prove it works. Book a free strategy call → We'll run your real customer prompts through the AI engines, show you exactly where you stand against competitors, and give you a clear next step within one business day.